Format of Balance Sheet: Schedule III & Key Notes Explained

For many commerce students, the balance sheet isn’t confusing because it’s complicated. It feels confusing because the structure looks rigid and unfamiliar. In India, companies cannot design their own layout for presenting their financial position. They must follow the format prescribed under the Companies Act, 2013, specifically, Schedule III.

Understanding the format of the balance sheet as per Schedule III is essential for B.Com students, CA aspirants, and anyone preparing final accounts. Once you understand the logic behind the structure, you won’t need to memorise placements. You’ll know why each item sits where it does.

This guide walks you through the Schedule III format step by step so you understand not just what goes where, but the reasoning behind it.

What Is a Balance Sheet?

A balance sheet is a financial statement that shows the financial position of a company on a particular date. It is prepared “as at” a particular date that is on 31st March 2025.

Unlike the Profit and Loss Statement, which measures performance over a period, the balance sheet is a snapshot. It answers three straightforward questions:

- What assets does the company own or control?

- What liabilities does the company owe?

- What portion belongs to shareholders?

Under Schedule III, it is formally referred to as the Statement of Financial Position, because it presents the company’s financial standing at a given point in time.

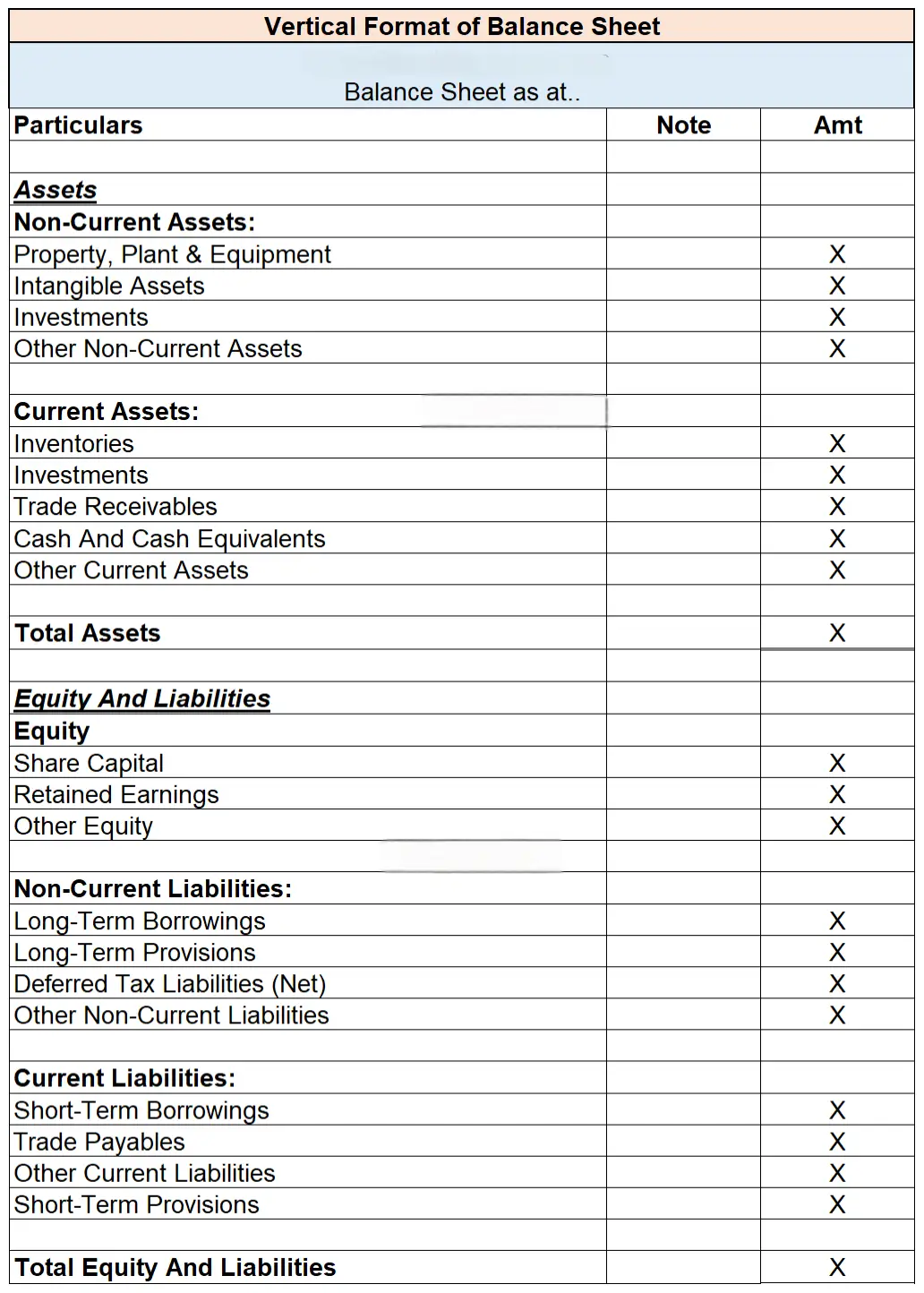

Overview of the Format of Balance Sheet as per Schedule III

The format of balance sheet of a firm as per Schedule III follows a vertical presentation. Items are listed one below the other, rather than side-by-side in a T-format.

The statement is divided into two broad sections:

- Equity and Liabilities – This explains the sources of funds.

- Assets – This shows how those funds are invested.

Within these sections, items are further classified into current and non-current based on the 12-month rule. If something is expected to be settled or realised within 12 months, it is current. Otherwise, it is non-current.

This classification improves clarity and helps users assess liquidity and long-term stability.

1. Equity and Liabilities

This section tells you how the business is financed.

A. Shareholders’ Funds

This represents the owners’ stake in the company. Although shown under liabilities, these amounts are not repayable in the normal course like loans. They represent the company’s net worth.

(i) Share Capital

Share capital is the money raised by the issue of shares. It reflects the initial and ongoing contribution of shareholders.

Under Schedule III, it includes:

- Equity Share Capital

- Preference Share Capital

The balance sheet shows the total paid-up amount. Detailed information-such as authorised capital, number of shares, face value, reconciliation during the year, and rights attached-is disclosed in the Notes to Accounts.

A common exam mistake is confusing authorised capital with paid-up capital or failing to adjust calls-in-arrears properly.

(ii) Reserves and Surplus

This head reflects accumulated profits retained in the business.

It typically includes:

- Securities Premium

- General Reserve

- Capital Reserve

- Surplus in Statement of Profit and Loss

Even if the balance of profit and loss is negative, it is still presented here-not shifted elsewhere.

Students often misclassify provisions as reserves. Provisions are obligations; reserves are appropriations of profit. The distinction matters.

B. Non-Current Liabilities

These are obligations due after 12 months from the reporting date.

(i) Long-Term Borrowings

These include:

- Term loans from banks

- Debentures

- Loans from financial institutions

Only the portion payable after 12 months appears here. The amount due within the next year must be shown under current liabilities.

This reclassification is frequently tested in exams.

(ii) Deferred Tax Liabilities (Net)

These arise from timing differences between accounting income and taxable income. Since settlement occurs in future periods, they are classified as non-current.

(iii) Long-Term Provisions

These are provisions expected to be settled after one year, such as:

- Provision for gratuity

- Provision for leave encashment

Separating long-term and short-term provisions ensures transparency about future obligations.

C. Current Liabilities

Current liabilities are payable within 12 months. They directly affect liquidity.

(i) Short-Term Borrowings

These include:

- Bank overdrafts

- Cash credit facilities

- Short-term loans

Even though overdrafts relate to bank accounts, they are not adjusted against cash balances. They are shown as liabilities.

(ii) Trade Payables

These represent amounts owed to suppliers for goods or services purchased in the normal course of business.

Schedule III requires separate disclosure of dues to MSMEs and other creditors.

(iii) Other Current Liabilities

This includes items such as:

- Outstanding expenses

- Advance from customers

- Unpaid dividends

- Current portion of long-term borrowings

Outstanding expenses are not provisions. They belong here.

(iv) Short-Term Provisions

These are provisions expected to be settled within 12 months, such as provision for income tax.

2. Assets

If the liabilities side shows “Where did the money come from?”, the assets side shows “Where is it invested?”

Assets are the resources controlled and managed by companies which are expected to generate future economic benefits.

A. Non-Current Assets

These are assets not expected to be realised within 12 months.

(i) Property, Plant and Equipment (PPE)

This includes tangible assets such as:

- Land

- Buildings

- Machinery

- Furniture

They are presented at cost less accumulated depreciation. The balance sheet shows the net carrying amount, while detailed movement is disclosed in notes.

(ii) Capital Work-in-Progress

Assets under construction that are not yet ready for use-for example, a factory building under construction-are shown here, not under PPE.

(iii) Intangible Assets

These are non-physical assets such as:

- Goodwill

- Software

- Patents

- Trademarks

They provide long-term benefits despite lacking physical form.

(iv) Non-Current Investments

Investments intended to be held for the long term, such as strategic equity investments or long-term bonds, are shown here.

(v) Long-Term Loans and Advances

Examples include:

- Security deposits

- Advance rent recoverable after one year

They are assets because they represent amounts recoverable.

(vi) Other Non-Current Assets

This head captures items like long-term prepaid expenses that do not fit elsewhere.

Also read- Deloitte USI Interview Questions for Chartered Accountants

B. Current Assets

These are assets expected to be realised, sold, or consumed within 12 months.

(i) Inventories

Includes:

- Raw materials

- Work-in-progress

- Finished goods

Valuation is done as per applicable accounting standards, with details in notes.

(ii) Trade Receivables

Amounts due from customers. Receivables outstanding for more than six months require separate disclosure.

(iii) Cash and Cash Equivalents

Includes:

- Cash in hand

- Bank balances

- Short-term highly liquid investments

(iv) Short-Term Loans and Advances

Such as:

- Prepaid expenses

- Advance tax

- Employee advances

Prepaid expenses are assets because the benefit will arise in future periods.

(v) Other Current Assets

Includes items like interest accrued but not yet received.

Checkout - Financial Statements Excel Template

Conclusion

The format of the balance sheet under Schedule III is structured, but it is not arbitrary. Every classification is based on either the nature of the item or the time frame in which it will be realised or settled.

Once you understand this logic, preparing or reading the format of balance sheet in final accounts becomes straightforward. Instead of memorising headings, you begin to think in terms of sources and uses of funds, current versus non-current classification, and disclosure requirements. That clarity is what turns the balance sheet format from a confusing statement into a logical financial document.

Also read- AI Tools and CHATGPT

About Author