- Key Takeaways

- What Exactly Is Auditing? (And Why Should You Care?)

- The Primary Objectives of Auditing with Examples

- The Secondary objectives of auditing with examples

- Scope and Objectives of Auditing Under SA 200

- Importance of Auditing: Why Does It Go Beyond Compliance?

- Primary vs Secondary Objectives of Auditing: A Quick Comparison

- Objectives of Auditing with Real-World Examples

- How the Audit Process Achieves Its Objectives: Step-by-Step

- Conclusion

- Frequently Asked Questions

- Ready to Master Auditing?

↓

Objectives of Auditing Explained with Examples

CA Archit Agarwal |

Fri, June 5, 2026

The objectives of auditing are to provide reasonable assurance that financial statements are free from material misstatement, whether caused by fraud or error, and to give an independent opinion on the financial statements. The secondary objectives of an audit are to detect errors, to prevent fraud, to ensure compliance with the laws, and to reinforce the internal controls.

Key Takeaways

- Overall objectives of auditing are defined by SA 200 (issued by ICAI).

- The main objective of audit is to render an opinion as to whether the financial statements are prepared fairly.

- Auditors do not provide absolute assurance, but only reasonable assurance.

- Secondary objectives include fraud detection, prevention of errors, compliance verification and management assistance.

- The materiality and audit assertions – existence and completeness, accuracy – influence the way auditors collect evidence.

- The auditor is not responsible for the preparation of the financial statements – that is management's responsibility.

- Every statutory auditor is required to have independence and professional scepticism.

What Exactly Is Auditing? (And Why Should You Care?)

Auditing is the independent, systematic application of professional scepticism and other audit techniques to obtain reasonable assurance that the financial statements of a company contain no material misstatements and are free of any material illegalities in order to express an opinion on whether they present a true and fair view of the organisation's financial position in accordance with the applicable financial reporting framework.

The Institute of Chartered Accountants of India (ICAI) established the Overall Objectives of the Independent Auditor (SA 200), which includes this information. In India, all statutory auditors must comply with these criteria when conducting audits.

Assume you offer your friend ₹5 lakh to start a business. A year later, you are handed a book of accounting. You can trust them, but you should double-check the numbers before taking out a new loan. The objective of Auditing is, in fact, independent verification at the corporate level.

According to a 2023 PCAOB (Public Company Accounting Oversight Board) study, audit failures occur most commonly when auditors are not expected to be cautious, such as when assessing management estimates and revenue recognition.

The NFRA (National Financial Reporting Authority), India's national authority in charge of inspecting audit companies, has regularly encountered non-compliance with the principles of SA 200 in its audit reports.

Understanding the objective of auditing is important for more than just exam preparation; they serve as the foundation for all auditing you will conduct as a CA.

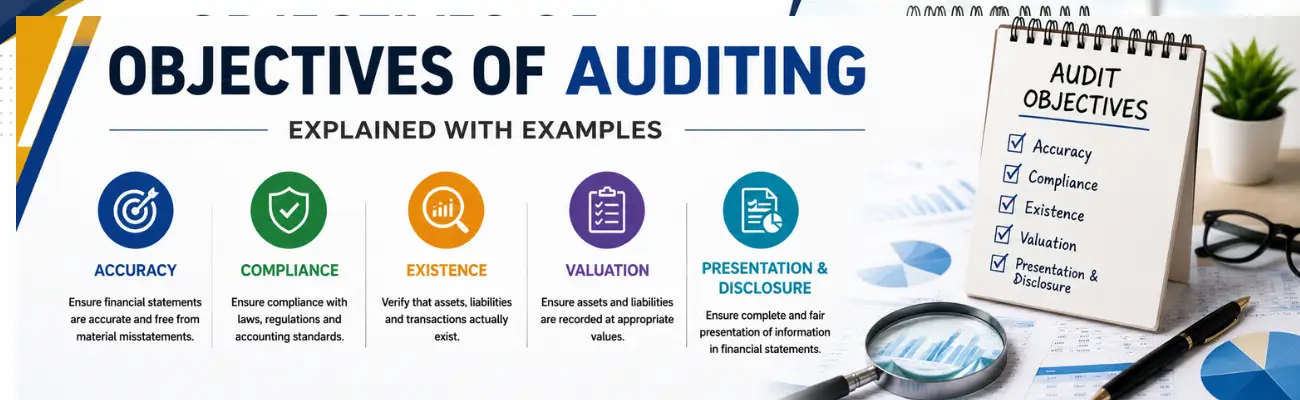

The Primary Objectives of Auditing with Examples

The overall purpose of auditing is to provide reasonable assurance that the financial statements, as a whole, are free from material misstatement, whether caused by fraud or error, and to report on the financial statements.

The first two phrases are of critical importance.

Reasonable assurance is not synonymous with absolute certainty. Auditors use samples, must make decisions and operate with flawed information. SA 200 is unequivocal that there can always be a risk of an undetected material misstatement. This is referred to as audit risk, which is the risk that the statements are materially misstated prior to the audit, or that the auditor is unable to detect the misstatement.

Material misstatement is an error or omission that is of a size or nature that would likely make a difference in the economic decisions made by financial statement users. The definition of “material” varies depending on the context: For a conglomerate, ₹10 lakh may be immaterial, while for a small private company, it may be very material. That is why auditors establish materiality thresholds when planning the audit.

What does the auditor's opinion actually say?

An audit report signed by the engagement partner at the end of a statutory audit provides an opinion of one of four types:

- Unmodified (Clean) opinion — statements are free from material misstatements.

- Qualified Opinion — if there is a specific matter, statements are fairly presented except for that specific matter.

- Adverse Opinion — statements are materially misstated and do not give a true and fair view

- Disclaimer of Opinion — The auditor has not been able to gather sufficient evidence to draw any opinion.

This opinion is targeted at shareholders, lenders, regulators and persons charged with governance (TCWG), which includes the board of directors and the audit committee.

A student may make a mistake in one thing: They think the auditor’s job is only to verify the financial statement, not to prepare it. Management's responsibility is to prepare financial statements under SA 200 and the Companies Act, 2013. The auditor reviews the documents prepared by the management.

The Secondary objectives of auditing with examples

Secondary objectives of the audit are to assist in the primary objective and to be of real value beyond opinion.

1. Detection and Prevention of Errors

Errors are unintentional misstatements in financial statements, which may result from wrong calculations, incorrect journal entries or misclassified expenses. They do not just occur in an audit; they are actively discouraged by a well-designed audit process.

Example: A medium-scale manufacturing firm had the wrongly capitalised expense of ₹8 lakhs for routine maintenance as fixed assets. This was identified in a vouching exercise by the statutory auditor and avoided an overstatement of profits and assets.

Types of Errors in Auditing - With Examples

Some errors are not the same. Auditors are trained to identify errors as they know where to look and what procedure to use. It is classified into 4 sections:

1. Error of Omission:

An entry is completely left out of the books, either on one side (partial omission) or both sides (complete omission). Completing omissions are more difficult to locate because the trial balance is not affected.

For example, a trading firm buys goods of ₹3 lakh from a supplier without taking note of it. The Trial Balance is still balanced, but purchases and creditors are overstated by ₹3 lakh. This is picked up by the auditor through creditor confirmation and GRN matching.

2. Error of Commission:

An entry is made, but the amount is entered incorrectly, the account is entered incorrectly, or the period is entered incorrectly. Both of these do impact an individual account balance, but do not affect the trial balance if either side has the wrong figure.

For example, if Customer A receives a receipt for ₹50,000 from Customer B, the receipt will be posted to Customer B's account. The total amount of debtors is correct, but each of the individual accounts is wrong. This would be immediately noticed by an auditor conducting debtor circularisation.

3. Error of Principle:

A transaction which has been recorded on the wrong accounting principle, most frequently, revenue expenditure has been capitalised (or capital expenditure recorded as revenue). These entries are in violation of the matching principle or the asset recognition criteria.

For example, the company incurs annual expenditure of ₹12 lakhs for whitewashing its factory, which it capitalises as a building improvement: It would overstate the value of the fixed assets and understate expenses, a mistake in principle. As per Ind AS 16, routine maintenance is not capitalised.

4. Compensating Errors:

Two or more errors that cancel each other out, leaving the trial balance unaffected. These are the ones that are the toughest to detect; they are not flagged by an imbalance.

For example, Sales are overstated by ₹1 lakh and purchases are also overstated by ₹1 lakh. The profit figure will not have changed, and the trial balance is still in balance. This would only be uncovered by detailed transaction-level testing or analytical review.

| Error Type | Affects the balance? | Affects profit | Detection Method |

|---|---|---|---|

| Error of Omission (partial) | No | Yes | Supplier confirmation and GRN matching. |

| Error of Omission (complete) | Yes | May be | Trial balance review |

| Error of Commission | Sometimes | Sometimes | Ledger inspection and circularisation |

| Error of Principle | No | Yes | Vouching and Classification Review |

| Compensating Errors | No | Sometimes | Analytical techniques, extensive tests |

The main distinction that examiners and interviewers look for is that errors of principle are the most damaging for financial reporting since they misrepresent the character of transactions rather than their numbers.

2. Detection and Prevention of Fraud

Fraud is defined as a deliberate misrepresentation, false records or misappropriation of assets or manipulation of accounts. In particular, SA 240 (The Auditor's Responsibilities Relating to Fraud) calls for auditors to exercise a high level of professional scepticism with regard to management's representations and to consider circumstances that may give rise to a risk of fraud.

For example, a bank auditor at a branch found an employee who had been using the facility to set up fake accounts and divert the small transaction fees for 18 months. This was highlighted by consistent analytical processes and by surprise cash counts.

The auditor need not necessarily be a forensic accountant, but they have to put procedures in place which provide them with a reasonable chance of detecting material fraud.

3. Verification of Compliance with Laws and Regulations

The statutory auditor in India is supposed to verify the compliance of the Companies Act 2013, applicable Accounting Standards (AS/Ind AS) and report as per CARO 2020 (Companies Auditor's Report Order). The listed companies are also subject to scrutiny by SEBI and MCA (Ministry of Corporate Affairs).

For example, under CARO 2020, the auditor has to give a particular observation on whether the company has failed to make any repayment of the loan to a bank or financial institution. This is a compliance-based goal that is directly linked to the audit report.

4. Ensuring a True and Fair View of Financial Statements

The term ‘true and fair view' is not only a term of art but a legal requirement pursuant to Section 129 of the Companies Act, 2013. If information is presented in a correct manner, it is a true view. Fair view is an absence of bias and an accurate representation of the economic substance of transactions.

For example, if a company incurs a contingent liability of ₹50 crore as a footnote to the financial statements but does not provide adequate information about the likelihood and impact of the contingent liability. Though it might be true and fair, an auditor who applied the true and fair view standard would need to make additional disclosure.

5. Assistance to Management and Stakeholders

The audit results, in particular management letters, provide the board and TCWG with information on areas of weakness, inefficiency and governance failings. These are not included in the formalised audit report, but rather are a useful spin-off of the audit process.

For example, the point is that the auditor discovered that 23% of SKUs had not moved in more than 12 months in the case of an internal audit of a retail chain. This led to a review of working capital and a complete revamp of the procurement process, which the finance team hadn't done internally.

Scope and Objectives of Auditing Under SA 200

The terms of the audit, as outlined in the terms of engagement or scope of the audit in the engagement letter (which is specified in SA 210) and the Standards on Auditing (applicable to the audit), influence the scope of an audit. There are no "no bounds" for scope; the auditor operates within certain limits.

Let's take a closer look at the connection between scope and objectives, step-by-step:

- Establish engagement goals: Statutory, internal, tax or special-purpose audit?

- Ensure terms are agreed in an engagement letter: Scope, timeline, fees, and responsibility

- Know the nature of the entity and its environment: SA 315 involves determining the nature and inherent risks of the entity and its environment, and control risks

- Establish materiality thresholds: Overall materiality, performance materiality and specific materiality for sensitive disclosures

- Design audit procedures: Tests of controls and substantive procedures based on the assertions

- Collect adequate relevant audit evidence: The quality and the quantity of evidence collected to support the opinion

- Write and deliver the opinion: Audit report to shareholders; Management letter to TCWG

Audit Assertions: The Hidden Architecture of Every Objective

Every goal eventually leads back to audit assertions, which are the claims that management implicitly makes when presenting a figure in the financial statements.

| Assertion | What it means | Example |

|---|---|---|

| Existence | Assets/liabilities actually exist | The inventory that is reported is the actual inventory in the warehouse. |

| Completeness | Nothing is omitted | All liabilities are taken into account, not only those which management wishes to demonstrate |

| Accuracy | Mathematically and factually correct amounts. | The revenue amount is the same as the revenue on the invoices and collections. |

| Valuation | There are correct quantities of items | Doubtful Debts are deducted from the value of Receivables. |

| Rights & Obligations | The company owns the assets / owes the liabilities | Land shown on the balance sheet is legally owned by the company |

| Presentation & Disclosure | Properly classified and disclosed. | Long-term debt is not recognised as current. |

These assertions serve as the prism through which an auditor assesses each line item on the financial statements. They are not simply conceptual; both the ICAI and the PCAOB include them in audit procedures and inspection checklists.

Importance of Auditing: Why Does It Go Beyond Compliance?

An audit is about more than just meeting regulatory requirements. This is why it is fundamental for the Indian economy and the global markets:

Builds Investor Confidence

An FII, PE fund or retail investor would never invest in a company that does not have its numbers verified independently. The audit opinion is the foundation of the integrity of the capital markets. There is a specific reason for the auditor rotation and independence disclosures mandated by SEBI for listed companies to strengthen this trust.

Detects Financial Crime

Even if financial statements are known to be going to an auditor, it is less likely to be manipulated. The potential of an audit is so much greater in preventing the problem than in detecting it.

Enables Credit Decision-Making

Loans are typically sanctioned in India based on audited financial statements that banks or NBFCs are accustomed to. Debt Covenant Reviews or Loan Calls will result if a qualified audit opinion is issued by a statutory auditor.

Supports Tax Administration

The Income Tax Act provides for tax audits for companies whose turnover exceeds certain levels under section 44AB. These audits help the Income Tax Department in the assessment process. In this regard, refer to our guide on income tax audit under section 44AB for a deep dive.

Governance and Accountability

The statutory auditor is one of the few independent safeguards to the board and management of companies regulated by the Companies Act, 2013. The NFRA has also made this happen through its independent supervision of auditors of listed entities and public interest entities, which was earlier only under the supervision of the ICAI.

To discover how the objectives are now practically being achieved with AI, check out our piece on artificial intelligence in audit.

Primary vs Secondary Objectives of Auditing: A Quick Comparison

| Parameter | Primary Objective | Secondary Objective |

|---|---|---|

| Defination | Obtain reasonable assurance; express an opinion on the financial statements | Detect errors, prevent fraud, verify compliance, assist management |

| Governed by | SA 200, Companies Act 2013 | SA 240, SA 250, CARO 2020, Income Tax Act |

| Output | Audit Report / Audit Opinion | Management Letter, CARO Report, Tax Audit Report |

| Focus | Financial statements as a whole | Specific transactions, controls, and compliance areas |

| Who Benefits | Shareholders, regulators, lenders | Management, TCWG, tax authorities |

| Nature | Mandatory for statutory audits | Some mandatory (CARO), some advisory |

Objectives of Auditing with Real-World Example

Only abstract concepts which are put to the test are remembered. There are four scenarios that CA students and professionals face frequently:

Scenario 1 — Reliance Industries (Statutory Audit context)

The statutory auditor of a large listed entity is required to check if revenue in thousands of contracts with customers is recognised in compliance with Ind AS 115. The goal of this would be to be accurate and complete on revenue, which is related to the assertion of occurrence and cut-off.

Situation 2 – Real Estate Developer (Compliance Audit)

The auditor has to report if the company has taken loans from related parties under CARO 2020 Clause 3(ix). This clause is triggered when a real estate developer takes a loan from a promoter-controlled NBFC. The goal is now shifted to verification and disclosure of compliance.

Scenario 3 — CA Articleship Firm (Internal Audit)

A pharma distributor's AR ledger is audited internally, and it is discovered that 18% of the debtors have outstanding debts of more than 180 days without provision. The goal here is value over stating that the debtors are not acceptable.

Scenario 4 — Tax Audit as per Section 44AB

A partnership firm whose turnover is more than ₹1 crore gets a CA who does a tax audit. The auditor will certify that TDS has been deducted and deposited in respect of all payments. The goal is compliance – compliance with the provisions of the Income Tax Act relating to TDS.

Knowing about these situations is the reason why you are prepared for an articleship interview. Read our article for practical tips on preparing for a statutory audit interview for CA articleship.

How the Audit Process Achieves Its Objectives: Step-by-Step

The first step is to know the goals. When you see how auditors actually get them, that's when you see it.

- Accept the engagement — Assess independence, competence and ethical needs prior to signing the engagement letter (SA 210)

- Perform the audit — Obtain and apply understanding of the entity, establish materiality and identify significant risks (SA 300, SA 315)

- Assess risk of material misstatement — Inherent risk × Control risk = Risk of Material Misstatement (RMM)

- Reduce substantive testing — Auditors can rely on strong internal controls.

- Carry out substantive procedures – Vouching, analytical procedures, confirmations, physical verification

- Assess evidence — Adequacy and appropriateness of evidence (enough, relevant + reliable)

- Make the opinion — Based on findings, conclude whether statements give a true and fair view or not

- Issue audit report (SA 260) – Communicate opinion to shareholders, communicate key audit matter to TCWG

Interested in knowing how to do a statutory audit in the real world? Our extensive statutory audit in CA guide will help you learn it from beginning to end.

Conclusion

The primary and secondary objectives of auditing are to make financial information trustworthy. The basic goal, as outlined in ICAI's SA 200, is to achieve reasonable assurance and provide an independent view. The secondary goals broaden the aim to include fraud detection, error avoidance, and compliance verification. They provide the foundation of financial accountability in all organisations, from small enterprises to SEBI-listed massive enterprises.

Frequently Asked Questions

1. What is the primary objective of auditing according to SA 200?

SA 200, published by the ICAI, describes the basic goal of auditing as getting reasonable confidence that financial statements are free of serious misrepresentation, whether owing to fraud or error and providing an opinion about such statements. The auditor's view improves the credibility of the financial accounts, but it does not ensure their complete correctness.

2. What is the difference between primary and secondary objectives of auditing?

The primary goal is to provide an unbiased evaluation of financial statements as a whole. Secondary objectives include identifying mistakes and fraud, ensuring compliance with legislation such as the Companies Act of 2013 and the Income Tax Act, and providing management with insights to strengthen controls. Both are pursued concurrently throughout an audit, but the primary goal dictates the overall scope and outcome.

3. What does "true and fair view" mean in auditing?

Section 129 of the Companies Act of 2013 establishes true and fair perspective as a legal and professional norm. "True" indicates that the information is factually correct and based on valid records. The term "fair" refers to an objective reflection of economic reality. If an auditor decides that the financial statements do not provide a true and fair perspective, he or she must offer a qualified or unfavourable opinion.

4. Is fraud detection an objective of auditing?

Yes, but with a condition. Fraud is a secondary concern, not the primary one. SA 240 requires auditors to create methods that have a reasonable risk of discovering significant fraud, particularly fraud that might result in a major misstatement. Auditors are not detectives; thus, there is a risk that some fraud, particularly collaboration, will go undetected even during a professional audit.

5. What is the scope of auditing?

The scope of auditing refers to the bounds of the audit, what the auditor will evaluate, how far the audit will go, and the criteria he or she will use. It is described in the engagement letter, influenced by the auditing standards applicable to the engagement (e.g., SA 200 and SA 210), and decided by materiality levels and risk assessments. This is not unlimited, but it is agreed upon at the start of the engagement by the auditor and management/TCWG.

6. How are audit objectives different for internal and statutory auditors?

A statutory auditor is appointed by the Companies Act of 2013 (or comparable law) and is primarily accountable to shareholders. Their purpose is to provide a viewpoint on financial data. An internal auditor is appointed by management and primarily reports to the board/audit committee. Their goals are broader, assessing risk management, governance, and operational efficiency, and they are not held to the same standards as statutory audits.

Ready to Master Auditing?

If you're studying for CA examinations or developing practical skills for getting articleship or jobs in a finance background, then the concept of the objective of an audit is essential. CA Archit Agarwal's Audit Masterclass covers SA 200 through SA 720, with real-world examples, interview and exam-focused explanations, and practical insights which are gained from actual audit engagements.

You can also explore:

About Author